The flood insurance gap in the United States is big and it’s not getting better. And the consequences of that gap are about to worsen for property owners and state and local governments, thanks to increasing rainfall amounts, stronger storm surge, more development in flood zones, cutbacks in federal aid, and aging river levees around the country.

That was the word from Moody’s Rating analysts who delved into the realities at a webinar Thursday.

“When flood losses happen and they are not absorbed by the shock absorber of insurance, they don’t disappear,” said Firas Saleh, director of insurance solutions and product management at Moody’s, the global ratings and analytics firm.

Some of those costs are shifted onto impacted households that do not carry adequate (or any) flood insurance, onto federal assistance programs, and—more and more—to state and local governments, Saleh said. Government programs often are asked to pay for debris removal, demolition of flooded structures, bridge replacement, road repairs and temporary housing.

But local property tax revenue often takes a dive after flooding events, as damaged sites lose value. That’s especially true in smaller, less-affluent counties and cities. The decline can affect local credit ratings, costing jurisdictions more to issue bonds and borrow money.

After Hurricane Harvey in 2017, for example, a few coastal counties in Texas faced deficits after properties were reassessed and property tax revenue plummeted, said Denise Rappamund, a vice president and senior analyst at Moody’s. Buncombe County, North Carolina, one of the places hit the hardest by Hurricane Helene flooding in 2024, saw its credit outlook rating temporarily downgraded to “negative,” explained Jennifer Chang, Moody’s Vice President and Senior Credit Officer.

As the current U.S. president and his administration have espoused major cuts in federal funding, including cuts to Federal Emergency Management Agency programs, it will fall more on cities, counties and state governments to rebuild infrastructure after devastating floods, the analysts said.

And locals may be less financially prepared than they have been in decades: Several states in recent years have reduced or eliminated their state income taxes, leaving smaller pots of money to handle greater losses. Florida lawmakers this year moved to cut much of the state’s property taxes for homeowners. If approved by voters, that could cost local governments as much as $12 billion a year, some economists have warned.

Some of the states that have most embraced the Donald Trump ideology of government spending reductions are the ones that will feel the pain the most: The deep red states of Texas, Louisiana, Florida, and North Carolina, for example, received the most federal disaster aid as a share of overall state revenue, from 2017 to 2025, the Moody’s team noted. Louisiana enjoyed the largest share in the country—more than 5% of its revenue came from federal disaster aid in recent years.

At the same time, participation in the National Flood Insurance Program has declined significantly in recent years, leaving some homeowners more exposed than ever, the Moody’s team pointed out. Some 470,000 NFIP policies were lost between 2018 and early this year. Since 2009, 5.6 million policies have left the program.

While private flood insurance firms have filled that gap to a large degree, the overall level of U.S. flood coverage has remained about the same, Saleh explained.

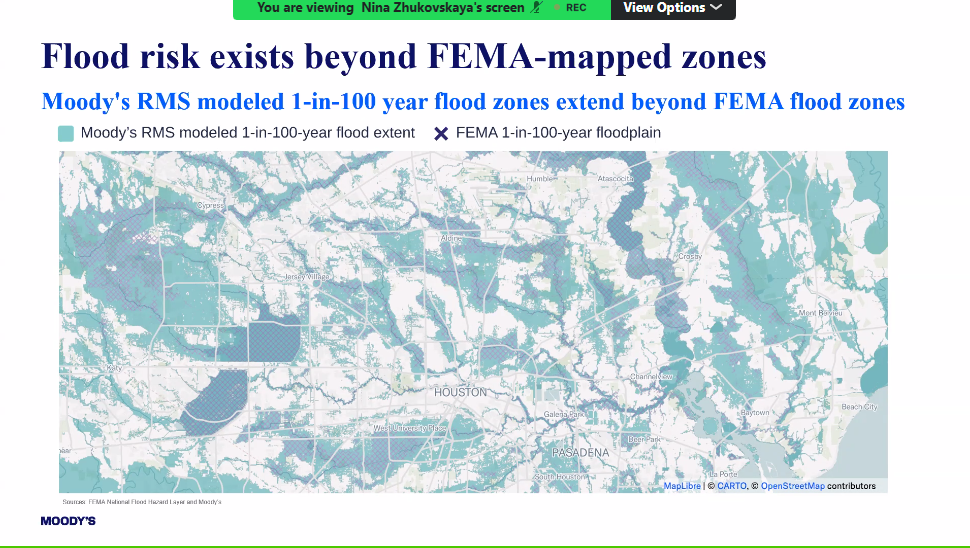

And while critics of the FEMA flood maps have long argued that the maps don’t show the true extent of flood-vulnerable areas, Moody’s computer models bring it into sharp relief. For the Houston area, for example, a Moody’s map shows a one-in-100-year flood reaching a vastly larger number of square miles than FEMA’s maps show.

The reach of inland flooding will be even greater if levees fail. Saleh said that studies show that America has about 100,000 miles of levees, mostly along rivers and lakes that may be increasingly vulnerable to extreme rainfall events.

The average age of those levees is 60 years old, he said.

How property-casualty insurers are preparing clients for these growing risks is less than clear and is something analysts and local governments will likely examine in coming months and years.

“There’s really a spectrum on how certain insurers are demonstrating what they are doing in terms of resilience, and how much they have invested,” Chang said.

Some carriers have developed plans to improve policyholders’ resilience to hazards, while others have not.

Moody’s published report on flood coverage can be accessed here.

Top photo: Flooding in downtown Annapolis, Maryland, in 2021. (AP Photo/Susan Walsh, File)

Was this article valuable?

Here are more articles you may enjoy.

Insurer Interest in AI Exclusions Growing as Risk Becomes Omnipresent

Insurer Interest in AI Exclusions Growing as Risk Becomes Omnipresent  Insurers Are ‘Actively Evaluating’ New Catastrophe Risks as Europe Burns

Insurers Are ‘Actively Evaluating’ New Catastrophe Risks as Europe Burns

Want to stay up to date?

Get the latest insurance news

sent straight to your inbox.