It’s every investor’s dream: Make money when markets go up, and when markets go down, and even when markets go practically nowhere.

But inside Allianz SE, where a handful of hedge fund managers claimed they could do just that, few grasped how wrong that dream could go. Four billion dollars wrong so far, with outside estimates that it could grow much larger.

Two years after the spectacular collapse of the insurance giant’s Structured Alpha hedge funds, a low-profile business registered in Florida, 5,000 miles from the Munich headquarters, the shock waves continue to reverberate.

Careers have been upended. Investor lawsuits and settlements have piled up. The U.S. Justice Department and Securities and Exchange Commission have opened investigations. Allianz in February set aside $4.1 billion for the disaster, but the final reckoning is still due — and could cost plenty more.

All these months later, the big question remains: How could a few obscure money managers — people on no one’s list of hedge-fund luminaries — blow such a huge hole in Allianz, which traces its history to the days of Bismarck? The answer that emerges from court filings, Allianz marketing materials and people with first-hand knowledge of Structured Alpha’s investment strategy is a classic story of Wall Street salesmanship and greed, and a tale for these volatile times.

No Wrongdoing

Allianz, which has denied wrongdoing, said earlier this month that independent advisers it’s hired to dig into what happened have thus far found no “breaches of duty” by the insurer’s management board. A spokesman declined to comment.

At the center of the debacle is Greg Tournant, 55, an equity-options whiz and one-time McKinsey & Co. consultant. A dual U.S.-French citizen, he arrived at Allianz Global Investors in the early 2000s by way of Oppenheimer Capital.

It turns out that Tournant and other fund managers behind Structured Alpha — including longtime colleague Trevor Taylor — previously ran into trouble during the 2008 financial crisis, with strategies that also involved options. Long before the pandemic, their small investment firm on Miami’s Brickell Avenue, aka, Wall Street South, collapsed when its trades went bad, according to two former employees there — foreshadowing what was to come. Tournant and Taylor declined to comment.

At Allianz Global Investors U.S., Tournant and his Structured Alpha team were incentivized to pursue outsized returns. Instead of employing the usual formula for hedge-fund fees — the “2 and 20” mix of management charges and a cut of profits — they were compensated for one thing alone: performance. The bigger the investment gains, the bigger the payday. While Allianz made no secret of this arrangement, angry clients would later claim it was a recipe for bigger risks.

Tournant himself was heavily invested in the funds he managed and lost money along with clients, according to a person familiar with the matter. In early March of 2020, as he was grappling with the pandemic’s effect on his funds, Tournant went on medical leave for undisclosed reasons, the person said. Structured Alpha’s troubles continued after his departure.

In the finger-pointing that followed, some big investors accused the professional consultants they had hired to vet Structured Alpha of ignoring red flags and failing to understand what the funds were doing, according to lawsuits.

Crashing Down

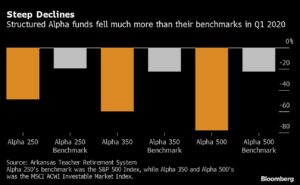

It all came crashing down in the early, panicked days of Covid-19, when wild market swings upended an options strategy that was marketed as “aiming to generate alpha regardless of market waves.” During the first quarter of 2020, five Structured Alpha funds lost between 49% and 97% of their value, performance that investors contend in legal filings was far worse than similar strategies.

Allianz, which also owns bond powerhouse Pacific Investment Management Co., has resolved some of its legal woes, including a February settlement with a majority of investors for undisclosed terms. At the same time, the firm has argued that its clients were sophisticated investors who knew what they were getting into.

The insurer continues to pick up the pieces. It fired Tournant and another fund manager, Stephen Bond-Nelson, in December, accusing them of violating compliance policies, according to public records filed with the Financial Industry Regulatory Authority. Bond-Nelson declined to comment.

Roman Frenkel was a first-hand witness to the Structured Alpha team’s earlier failure when he worked at Innovative Options Management, the small Miami firm that Taylor founded and Tournant helped run briefly while continuing to manage money for Allianz. Disaster struck in 2008 when the collapse of Lehman Brothers rocked global finance, freezing up markets — and with them, Innovative Options’ trades.

“The over-the-counter spreads were so great, they couldn’t close positions,” said Frenkel, who was chief compliance officer for Innovative Options. Instead of being part of the company’s planned expansion to waterfront offices, Frenkel ended up helping liquidate the business.

Solid Performance

Tournant and Taylor prospered at Allianz during the long bull market that followed the Great Recession. Deep-pocketed investors piled in. They included dozens of public and private pension plans for the likes of Blue Cross & Blue Shield and New York’s Metropolitan Transportation Authority.

Structured Alpha’s performance was solid. Its Alpha U.S. Equity 250 fund posted average annual returns of 10.9% between early 2005 and June 2018, compared with the S&P 500’s 8.7% average annualized return over the same period, according to a 2018 marketing document.

Allianz was confident enough in Tournant’s team that it let them charge a performance fee alone of 25% to 30% of net capital appreciation above a benchmark.

Notably, as markets got more volatile, the funds could get more profitable, Allianz told clients, while warning that all investments entail risks. Allianz also assured investors that it was backstopping Structured Alpha’s risk-management processes. By December 2019, Structured Alpha had grown to more than $10 billion, according to a person familiar with the matter.

“Every single time we greatly benefited from the higher levels of volatility and were able to generate much higher returns in the following two or three months after the draw-down,” Tournant said in a 2016 marketing video.

Abandoning Controls

But when the pandemic hit, everything went haywire. Investors allege Allianz and Structured Alpha abandoned risk controls and turned a challenging situation into a disaster by doubling down on a bad strategy.

That’s according to the Arkansas Teacher Retirement System, which in February settled a suit over its Structured Alpha losses for $643 million.

Another investor, the board of a pension fund run by the International Brotherhood of Electrical Workers, filed a lawsuit in 2020 that purported to identify what went wrong. The board alleged that when the pandemic started fueling wild volatility in February, Structured Alpha made a fateful bet against further market declines. It did so by selling options that would pay out for the purchasers, and hurt Structured Alpha, if the S&P 500 plunged, the pension said.

The trade proved disastrous for the Allianz fund managers when the index tanked in late February, and global markets experienced their largest single-week declines since the height of the 2008 financial crisis, the board claimed. By the end of March, Allianz announced it was liquidating two Structured Alpha funds.

Allianz is still grappling with the fallout. The insurer warned last month that ongoing probes by the Justice Department and SEC are at a “sensitive” stage and it couldn’t yet predict the final price tag from regulatory settlements and private litigation. Bloomberg Intelligence analysts predicted Feb. 18 that the insurer’s 3.7 billion euro provision won’t likely be sufficient and that its legal costs might approach $6 billion.

Compensation Hit

Chief Executive Officer Oliver Baete expressed regret in February for Structured Alpha’s losses and said they will have a “significant impact” on the compensation of its directors.

The funds’ writedown will put a costly end to what Allianz once described as a “‘third way’ for investors to harvest sustainable alpha.”

–With assistance from Stephan Kahl.

Was this article valuable?

Here are more articles you may enjoy.

Bodily Injury Is Now A Big Share of Auto Claims Payouts. Is AI to Blame for That Too?

Bodily Injury Is Now A Big Share of Auto Claims Payouts. Is AI to Blame for That Too?  Amazon’s Zoox to Levy Fares, in US First for Controls-Free Taxis

Amazon’s Zoox to Levy Fares, in US First for Controls-Free Taxis  AI Skills More Valuable Than MBAs, 86% of Finance Executives Say

AI Skills More Valuable Than MBAs, 86% of Finance Executives Say  Hackers Hit Bitcoin’s Safest Hiding Place in Ongoing Attack

Hackers Hit Bitcoin’s Safest Hiding Place in Ongoing Attack

Want to stay up to date?

Get the latest insurance news

sent straight to your inbox.