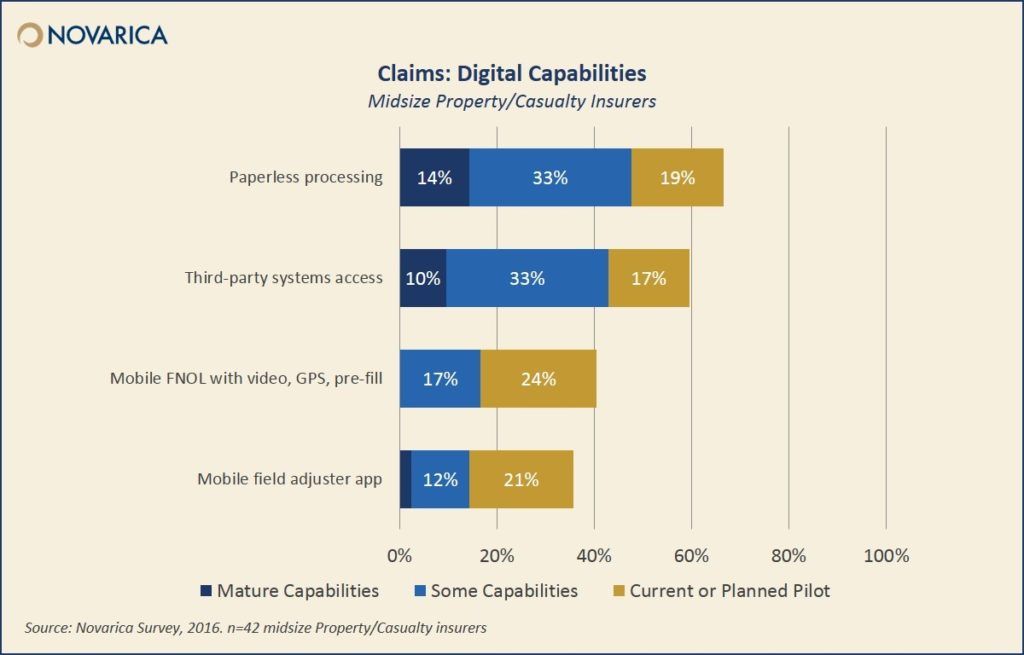

A report released earlier this year by research and advisory firm Novarica highlights how digital opportunities, analytics and the Internet of Things (IoT) are driving changes in claims.

Customer service standards set by other industries is contributing to the digital transformation in the insurance industry and in claims, stated the report, The Digital Evolution of P/C Claims.

Insurers are examining emerging technology, like IoT, telematics, blockchain, UBI, mobile, wearables, sensors, GPS, drones and smart fabrics, the reported noted.

In addition, insurers are leveraging big data and analytics to streamline processes and improve user experiences.

A recent article by data and software firm SAS cites six areas where data analytics can improve claims handing:

- Fraud

- Subrogation

- Settlement

- Loss Reserve

- Activity

- Litigation

Rather than having to rely on gut instincts, adjusters can use predictive analysis which “uses a combination of rules, modeling, text mining, database searches and exception reporting to identify fraud sooner and more effectively at each stage of the claims cycle,” the author of the SAS article wrote.

Another area that can benefit from analytics, is activity or assignment of loss where the use of data can more precisely match the best adjuster for the claim.

Digital Adoption

According to Keith Raymond, vice president of Research and Consulting, and co-author of Novarica’s report, digital isn’t just about mobile or omni-channel capabilities.

Rather, he said it encompasses “all of the processes required to fulfill an external request from an agent or broker through the back-end processes triggered during moment-of-truth interactions with carriers. The resulting expectations require insurers to rethink the relationships between information, people, and processes given new capabilities.”

CSC, a global provider of next-generation IT services and products and 360Globalnet, a UK-based digital insurance solutions provider, announced a new relationship this week, which includes a strategic investment by CSC in 360Globalnet.

CSC, a global provider of next-generation IT services and products and 360Globalnet, a UK-based digital insurance solutions provider, announced a new relationship this week, which includes a strategic investment by CSC in 360Globalnet.

CSC said it will provide systems integration services for 360Globalnet’s self-serve digital claims technology that includes intelligent systems, smart mobile devices, live-streaming video, data analytics and fraud detection.

“What if everyone involved in the settlement of a claim, from the first notice of loss to repair, had all the real-time data they needed in front of them – text, images and video – moments after it occurred?” asked Paul Stanley, 360Globalnet CEO. “Seamless, real-time visibility across the claims process is a winning proposition for insurers that can be implemented with low up-front costs, minimal disruption to existing software and short implementation times.”

DropIn, an LA- based startup, created a service that it says can reduce claims processing time from 10-12 days to less than 24 hours. Insureds can use a video streaming service that relies on smartphone cameras for auto accidents, or drones for property damage, to record damage in real time.

Snapsheet, is another company that offers similar self-service, virtual claims handling to insurers.

Other companies, like Nexar and TrueMotion, have created products insurers can use to pull telematic data from sensors in smartphones. Nexar also uses a dashcam app, powered by artificial intelligence, to create driving scores based on a driver’s behaviors on the road, that insurers can use to craft personalized policies. Detailed accident reports can be generated instantly.

Embracing IoT

According to a report by Ernst & Young released last year, The Internet of Things in Insurance: shaping the right strategy, managing the right risks, IoT is expected to move claims to a more active loss prevention role. Sensors on appliances and in the home can monitor for fire, wind and water damage, the paper’s authors wrote. Just this week, Wallflower Labs announced the release of its Smart Monitor for electric stoves.

In addition, in-vehicle sensors can warn of dangerous driving patterns in real time.

The impact of this direct connection to customers, according to the E&Y report, is that insurers will gain a better understanding of their policyholders and their coverage needs and can then offer more personalized products.

Was this article valuable?

Here are more articles you may enjoy.

Ex-Red Lobster Owner Says in Lawsuit Defense That Endless Shrimp Not Its Idea

Ex-Red Lobster Owner Says in Lawsuit Defense That Endless Shrimp Not Its Idea  Insurer Interest in AI Exclusions Growing as Risk Becomes Omnipresent

Insurer Interest in AI Exclusions Growing as Risk Becomes Omnipresent  Google Ordered to Defend Conservative Activist Starbuck’s AI Defamation Suit

Google Ordered to Defend Conservative Activist Starbuck’s AI Defamation Suit  Instagram, Facebook Ran AI ‘Nudify’ Ads from China, NGO Says

Instagram, Facebook Ran AI ‘Nudify’ Ads from China, NGO Says

Want to stay up to date?

Get the latest insurance news

sent straight to your inbox.