Is this claimant supposed to be off work? Did I get enough discount on the services? Were those services even necessary? I would argue that the question everyone should be asking instead is: Who is your doctor? After all, the physician is the person who sets all of the other wheels in motion — wheels that influence things from quality of care to how long an employee is out of work and the ultimate cost of an injury.

Throughout the past 15 years that I’ve spent managing networks and working with top companies developing custom solutions, one thing has consistently held true: physician quality matters … A LOT. In fact, provider quality is shown to make the single greatest impact on a claim. It’s something that shouldn’t be overlooked, and yet all too often it is.

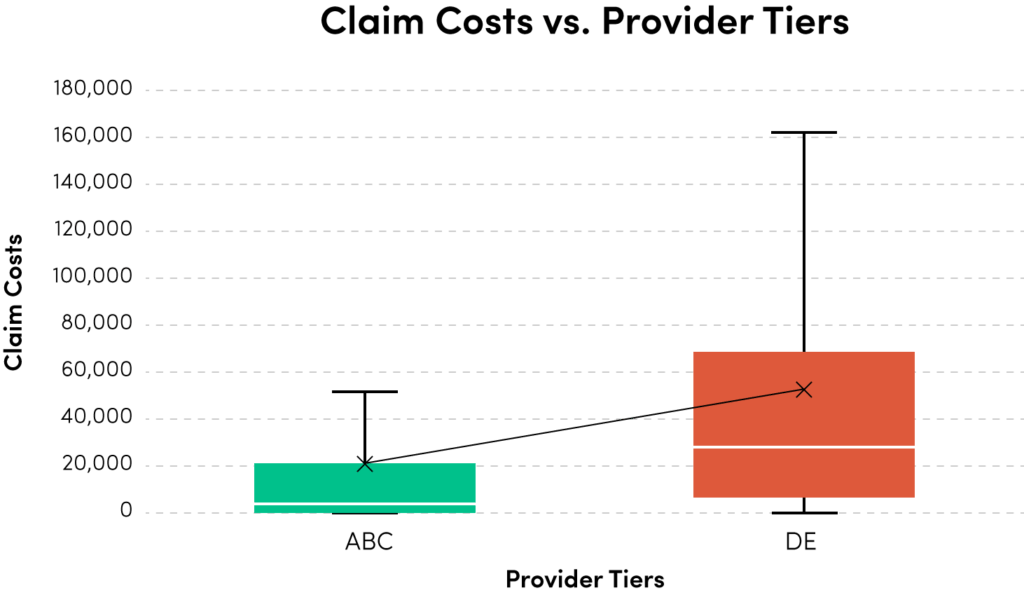

Numerous studies have shown that good doctors make a difference. There is a huge discrepancy in claims associated with doctors who score well on an outcomes basis versus those who don’t. The average costs associated with a problematic D or E-rated physician, compared to a rock star A or B-rated doctor, are astounding when you really dig into the data.

It is even more profound when you factor in case mixing and adjust results based on severity or type of claim.

A wealth of information now exists on physician quality, and many different models, from simple to complex, can provide useful insights into which doctors can be associated with better outcomes. Carriers and employers should apply this data to think more aggressively about their networks.

The PPO Dilemma

Before we get there, however, let’s look at what’s going on with PPOs. PPOs are the most common strategy utilized to impact costs in our market. A PPO’s value comes from providing a negotiated discount on a medical encounter. Once you have entered into business with the PPO, its primary revenue source comes from matching your bills to a pre-negotiated discount — and they get more matches by contracting with more doctors. Therefore, if they only contract with the best outcomes doctors, they lose significant amounts of revenue any time bills come in from uncontracted doctors that don’t perform as well in outcomes.

As such, all discount networks must contract with as many doctors as possible to assure they don’t lose revenue by missing a hit on a bill. A perfect PPO would include 100 percent of doctors who pass the base qualifications of credentialing. As shown in the prior illustration, there is a huge difference in outcomes between the top half and bottom half of the PPO’s doctors. I don’t fault PPOs for this — PPOs do offer a clear value in reducing purchase costs per episode. They also must contend with multiple factors from jurisdiction to jurisdiction that will always limit how “choosy” they can be. There is a role to be played by discount networks, but that role is not the full picture of how to bend the curve on claim costs.

“Savings” Don’t Always Reduce Costs

Here is a simple concept: If a cheap pair of shoes costs 30 percent less than a high-quality pair, I might save money on the initial purchase, but if the cheaper pair of shoes needs to be replaced twice as often, my savings on each transaction doesn’t lower my total shoe cost.

Applying this logic to medical care, let’s look at two patients — one going to a discounted doctor and one going to a full-fee schedule doctor. Let’s assume a typical ratio of 7:5 visits between high scoring and mid-tier doctors (the real difference is typically higher). Patient A goes to an in-network doctor selected at random from an approved list of providers that generates a five percent savings off each bill. Patient B is sent to a doctor with a high outcome score but no discount. The average bill from each doctor is $100. After the first visit, Patient A has cost $95 and Patient B has cost $100. The payer for Patient A saved $5, and the payer for Patient B has saved $0. By the time Patient A has been to his/her seventh and final visit, medical care cost $665, with PPO savings of $35. Patient B’s care wrapped up after five visits, costing $500, with $0 in PPO savings. This showcases the problem of using percent of savings as a metric – longer duration and $165 more in total medical costs reflects $35 in savings over Patient B. The metric is flawed because the more you spend the more you save.

The point to consider is that network savings are the shiny object that distracts from the difference in total costs. I am not arguing against leveraging savings where available; rather, I want to underscore that quality at a higher price point can significantly outpace discounts when you look at the total cost of a patient in any market.

All health markets suffer from the cost of care that requires too many visits or the additional costs of a second necessary procedure to repair a bad surgery. In workers’ comp, this is exponentially compounded when you factor in the costs of temporary disability as a result of poor recovery and permanent disability stemming out of failed procedures.

The Path Forward

The best way to start down the path forward is to separate the decision about which doctors to work with from how to work with them. The who should be determined by some level of quality metric while the how is figuring out which PPO or contractual relationships get you the best access to doctors who will get you the best results. This means you should first find the doctors that perform well on your chosen metrics, and then look at the PPO or combination of PPOs that get you contractual access. It works in the opposite flow as well; you can look at the total population of doctors available through your network vendors, then pick who you want to work with from that list.

In part two of this series, I will go into the concept of right-sizing networks and the relationship between PPOs and Exclusive Provider Organizations (EPOs). Pick the doctor, and then figure out which network or combination of networks provides access. It may require a little more work and data science on the front end, but the outcome is well worth it.

Gregory Moore is chief commercial officer of CLARA analytics, a predictive analytics company for workers’ compensation. Prior to joining CLARA analytics, Moore founded Harbor Health Systems, which he led for 16 years. During his time at Harbor Health, he pioneered many aspects of outcomes-based network models and brought provider benchmarking into the mainstream for workers’ compensation insurance and managed care companies. For more information, visit www.claraanalytics.com/ and follow CLARA analytics on LinkedIn, Facebook and Twitter

Gregory Moore is chief commercial officer of CLARA analytics, a predictive analytics company for workers’ compensation. Prior to joining CLARA analytics, Moore founded Harbor Health Systems, which he led for 16 years. During his time at Harbor Health, he pioneered many aspects of outcomes-based network models and brought provider benchmarking into the mainstream for workers’ compensation insurance and managed care companies. For more information, visit www.claraanalytics.com/ and follow CLARA analytics on LinkedIn, Facebook and Twitter

Was this article valuable?

Here are more articles you may enjoy.

Wildfires Destroy Hundreds of Structures in Washington State

Wildfires Destroy Hundreds of Structures in Washington State  Hims & Hers Sued by FTC, Utah in Federal Court

Hims & Hers Sued by FTC, Utah in Federal Court  Instagram, Facebook Ran AI ‘Nudify’ Ads from China, NGO Says

Instagram, Facebook Ran AI ‘Nudify’ Ads from China, NGO Says

Want to stay up to date?

Get the latest insurance news

sent straight to your inbox.