The Florida Hurricane Catastrophe Fund is well equipped to handle losses from Hurricane Ian, which are now estimated to cost the fund about $10 billion, but it could mean the fund will have borrow billions next year – at steep interest rates.

“We’ve been here before. We’re going to do what we’ve always done, and we’ve done it well,” Gina Wilson, chief operating officer of the cat fund, said at a fund advisory council meeting this week. “We are well-prepared for Hurricane Ian and we can cover our obligations.

A claims-paying capacity report from the Raymond James investment banking firm, which advises the cat fund, backed up Wilson to a large degree. But it also indicated that the fund’s surplus could fall short next year, even without another storm.

“After adjusting for Hurricane Ian loss estimates, the FHCF has liquid resources that are significantly below its statutory limit for the subsequent season,” reads the report, presented by Kapil Bhatia of Raymond James.

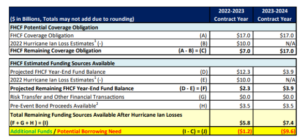

The report shows that the cat fund will likely need to borrow as much as $1.2 billion this year and another $9.6 billion for the 2023-2024 contract year to meet its statutory obligations.

“The projected 0-12 month bonding capacity of $8.4 billion allows for the FHCF to fund a majority of its maximum statutory obligation, but additional funding sources are needed to fund its statutory limit of $17 billion for the 2023-2024 Contract Year,” the Raymond James analysis said.

“The projected 0-12 month bonding capacity of $8.4 billion allows for the FHCF to fund a majority of its maximum statutory obligation, but additional funding sources are needed to fund its statutory limit of $17 billion for the 2023-2024 Contract Year,” the Raymond James analysis said.

And while the cat fund can lay a surcharge on Florida policyholders if needed, and has an excellent credit rating, it’s not guaranteed by state government. Given the current volatility of the global market now, along with rising interest rates and inflation, the cat fund could expect to pay bond interest rates as high as 7% to 9%, Bhatia said.

The report’s findings appear to give some credence to warnings raised earlier this month from analysts who fear that issuing bonds could be prohibitively expensive for the fund and would ultimately mean less cat fund reinsurance for Florida property insurers.

The principal and interest on new debt would mean “they never build surplus – even with no losses,” said Ian Gutterman, of Chicago, founder of a startup insurance company and a longtime insurance industry analyst and blogger. “There would be years with no debt maturities where surplus would temporarily build but then it would be drained by the next maturity.”

In other words, a bond buyer would have to assume either no more hurricanes will strike Forida for as long as the debt is outstanding, perhaps 10 years, or if there is one, the state of Florida will make good on the bonds if the cat fund doesn’t have the resources, Gutterman said.

“But there is no path for the FHCF on its own to both pay a future hurricane claim AND pay back bondholders,” he argued. “The debt can get you through, but the debt has to be paid back. And if you have more hurricanes, what do you have to pay the debt back with?”

The crux of the issue is that the fund’s diminished liquidity could force some insurance companies to seek more reinsurance coverage from the private market. With reinsurance prices expected to rise again next year, that could lead to lowered financial ratings and could doom a number of insurers that are now teetering, Gutterman and others have said.

The cat fund analysis underscored the problem of escalating reinsurance costs.

“Due to Hurricane Ian losses and global macroeconomic factors, the global reinsurance markets are expected to harden further, which will further reduce the reinsurance capacity for the Florida market,” the Raymond James report said.

John Rollins, an actuary and former chief financial officer for a large Florida insurance carrier, also questioned some of the cat fund’s recent assumptions, highlighted in the Raymond James analysis.

“The first question is, how lucky do Florida leaders feel about each of those ‘no shock’ assumptions?” he wrote on his Linkedin page. “Irma loss estimates have proved low at each milestone, and the fund must commute with 100+ individual insurers by June 2023 to determine the final tally.”

The Raymond James review also noted that the retention level – the deductible that insurers must pay before they can tap into the cat fund’s low-cost reinsurance – will rise to $9.1 billion for next year, up from $8.5 billion.

“Can insurers survive an inflation of the retention to $9.1 billion next year and an increase in premiums to $1.6 billion next year, or will legislators reform the fund and reduce premiums?” Rollins asked.

Florida Gov. Ron DeSantis said this month that he will convene a special session of the Legislature, probably in late November or early December, to tackle some of the most pressing issues still facing Florida insurers. Lowering the retention level on the cat fund has been discussed for years as a way to save Florida insurers on their reinsurance costs. But it’s not yet clear if that will be on lawmakers’ agenda. Other ideas include outlawing assignment-of-benefits agreements, a move that could stem the number of claims lawsuits filed in Florida.

Others have suggested that Ian’s impact won’t be so drastic. The cat fund won’t have to pay all of its reimbursement obligations at once but will likely space payments out over the next several years.

Wilson, the cat fund’s COO, told the advisory council meeting that for Hurricane Irma, in 2017, and Michael in 2018, FHCF has incurred losses of $9.25 billion but has not quite finished paying on that. The fund has paid 137 insurers for losses in the two storms, but expects to reimburse about seven more carriers.

Wilson also said that no insurers have yet requested reimbursement for Hurricane Ian losses. But when they do, the fund should be able to pay quickly.

The $10 billion projected cat fund loss from Hurricane Ian, which made landfall in southwest Florida on Sept. 28 of this year, is a “conservative point” in a range arrived at by the cat fund’s consulting actuary, based on a range of factors, the Raymond James report noted. The actuary, Paragon Strategic Solutions, has estimated that FHCF’s share of losses will be between $4 billion and $12 billion.

“There is significant uncertainty regarding the ultimate loss amount as losses are just beginning to develop,” the Raymond James analysis said. “Estimates are based on the output of models and are subject to significant uncertainty; therefore, there is no guarantee that actual losses will fall within the projected range.”

Was this article valuable?

Here are more articles you may enjoy.

Founder of Auto Parts Maker Charged With Fraud That Wiped Out Billions

Founder of Auto Parts Maker Charged With Fraud That Wiped Out Billions  US Will Test Infant Formula to See If Botulism Is Wider Risk

US Will Test Infant Formula to See If Botulism Is Wider Risk  Canceled FEMA Review Council Vote Leaves Flood Insurance Reforms in Limbo

Canceled FEMA Review Council Vote Leaves Flood Insurance Reforms in Limbo  Hackers Hit Sensitive Targets in 37 Nations in Spying Plot

Hackers Hit Sensitive Targets in 37 Nations in Spying Plot

Want to stay up to date?

Get the latest insurance news

sent straight to your inbox.