View this article online: https://www.claimsjournal.com/news/southeast/2018/09/19/286829.htm

Hurricane Florence may be just the first of several major storms to make landfall in the U.S. during hurricane season in 2018, but it’s impact will be significant.

As of noon on Saturday, more than 30 inches of rain had fallen on Swansboro, N.C., breaking the statewide rainfall record set by Hurricane Floyd in 1999 of 24.06 inches.

Florence is also being compared to two other catastrophic hurricanes that hit the Carolinas – Hurricane Hazel in 1954 ($15B in losses) and Hurricane Hugo in 1989 ($20B in losses). And, perhaps more concerning are the similarities being drawn between Florence and Superstorm Sandy and Hurricane Harvey. A weakened jet stream and warmer ocean temperatures mean Florence is moving slowly, similar to what happened for both Superstorm Sandy ($70.2B in damages) and Hurricane Harvey ($125B in damages). A study released in the science journal Nature in June found that tropical cyclone translation speeds had slowed by 10 percent worldwide between 1949 and 2016, resulting in storms lingering longer than before and much higher rainfall totals.

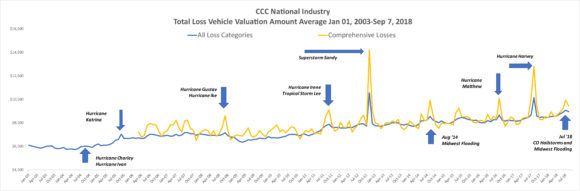

Analysis of the significant surge in the volume of total loss valuations from Superstorm Sandy and Hurricane Harvey shows volume was 20-30 times higher than the comprehensive total loss volume for the same period in years prior. Applying this type of increase to total loss volumes for North Carolina and South Carolina alone suggests the industry may see tens of thousands of total loss vehicles from Florence alone.

Comparison of the average total loss value for Sandy and Harvey also suggest that the total loss claim costs themselves could be as much as 50 percent higher than the non-comprehensive total loss average claim cost. The combination of a significant lift in volume as well as average loss amount suggests the impact to overall national total loss costs might be as dramatic as that seen from Harvey and Sandy.

Outside of vehicle losses, overall losses for the insurance industry for other lines of coverage may end up being less than in other major storms. Losses from inland flooding (one of the biggest concerns based on current conditions) do not fall under a standard homeowner’s insurance policy, but rather is covered via flood insurance. The U.S. flood insurance program, administered through FEMA, covers about 5 million policyholders in the U.S., but remains $20 billion in debt. $120 billion disaster relief was approved by Congress for last year’s hurricanes and wildfires, as well as $16 billion in debt accrued by the National Flood Insurance Program (NFIP). The House passed a new bill, the 21st Century Flood Reform Act (H.R. 2874), to make changes to national flood program last year, but Senate has not acted on the bill.

Currently there are about 444,000 NFIP policies in force in North Carolina, South Carolina and Virginia, but most are located in the Special Flood Hazard Areas on the NFIP Flood Insurance Rate Maps; there are very few insured properties outside the mapped flood plains. And, according to a recent ranking of individual state’s building code from the Insurance Institute for Business and Home Safety, South Carolina’s rules are among the most up to date among hurricane-prone states, but North Carolina’s code lagged behind the rest of the country by one or two cycles and didn’t meet even the 2009 standards for anchoring windows and doors.

Clearly the scope, scale and conditions predicted for Florence will mean significant losses across the Southeast, particularly in the Carolinas. And perhaps most worryingly, there are three other tropical storms building in the Atlantic – making 2018 the first year since 2008 where the Atlantic is seeing four names storms at the same time. The Atlantic hurricane season may yet turn out to be an above-average year.