View this article online: https://www.claimsjournal.com/news/national/2017/05/09/278348.htm

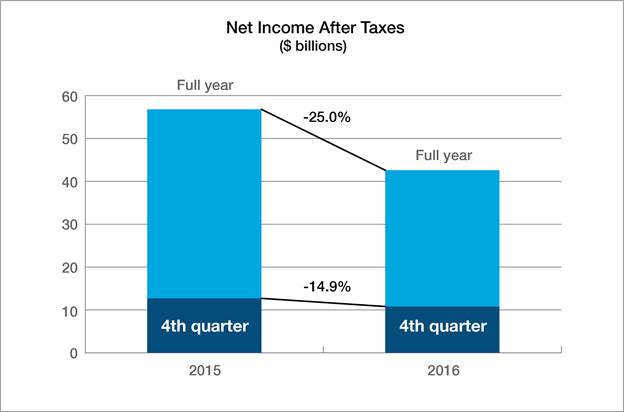

Private U.S. property/casualty insurers suffered a $4.7 billion net underwriting loss in 2016-following an $8.9 billion net underwriting gain in 2015-and experienced a 25 percent drop in net income after taxes to $42.6 billion from $56.8 billion a year earlier, according to ISO, a Verisk Analytics business, and the Property Casualty Insurers Association of America (PCI).

Insurers’ combined ratio deteriorated to 100.7 percent in 2016 from 97.8 percent in 2015, and net written premium growth slowed to 2.7 percent in 2016 from 3.5 percent a year earlier. Net investment income dropped to $46.3 billion in 2016 from $47.2 billion in 2015, and realized capital gains decreased to $7.3 billion from $9.4 billion, resulting in $53.7 billion in net investment gains for 2016, down $3.0 billion from a year earlier.

Direct insured property losses from catastrophes striking the United States totaled $21.6 billion in 2016, up from $15.2 billion a year earlier and above the $19.2 billion average direct catastrophe losses for the past ten years.

“Catastrophe losses continued to hurt insurer performance in 2016. There were 43 catastrophe events in 2016, the highest number of such events since 1980. There’s no way around it-to underwrite catastrophic risk better, insurers need detailed and accurate analytics of weather and environmental perils. But last year’s catastrophe losses weren’t the only ones that affected insurers. Legacy losses also continued to hurt performance and were evidenced by reserve charges and several special reinsurance transactions designed to limit the development of carried reserves. Those legacy issues should serve as a strong reminder that insurers need to engage in disciplined underwriting now or pay the price for it later. Those insurers that use robust data and up-to-date policy language will be the best poised for success,” said Beth Fitzgerald, president of ISO Solutions.

Commercial lines direct written premiums expanded to $258.6 billion in 2016, a 3.1 percent increase from a year earlier, according to estimates from ISO MarketStance. The increase in direct premiums was mostly the result of exposure growth in small commercial and middle market risks, such as specialty trade contractors, building construction, real estate, and auto dealers.

“Industry operating results during 2016 continued to hover near long-term trend lines-although with deterioration since 2013 in almost all categories, including premium growth, incurred loss and loss adjustment expenses, underwriting gains, and pretax income. Results were dragged down in part by soaring losses in personal and commercial auto, where accident frequency and severity continue to outpace premium increases and evidence suggests adverse development in reserves. Net investment income also worsened to the lowest level in decades, reflecting a long-term decline in net yield on invested assets. Despite the recent headwinds, policyholder surplus continued its steady growth to record levels, boosted by an increase in unrealized capital gains. But direct and net written premium increases since the last recession have still significantly lagged behind policyholder surplus and GDP growth,” said Robert Gordon, PCI’s senior vice president for Policy Development and Research.

Insurers’ net income after taxes fell to $10.8 billion in fourth-quarter 2016 from $12.7 billion in fourth-quarter 2015, and their combined ratio worsened to 104.1 percent in fourth-quarter 2016 from 100.4 percent a year earlier.

Their annualized rate of return on average surplus dropped to 6.2 percent in fourth-quarter 2016 from 7.6 percent a year earlier.

Net written premiums rose $2.9 billion, or 2.4 percent, to $124.4 billion in fourth-quarter 2016 from $121.5 billion in fourth-quarter 2015.